How to Budget – 7 Simple Steps to build a Successful Budget – Create a budget to achieve financial goals using a spreadsheet.

Budgeting is an essential skill that is required to save money, pay off debt, or reach financial independence.

Without knowing how to budget, it can be difficult to improve your financial situation.

In this post, I will cover how to budget money to achieve financial goals by using simple calculations and a simple spreadsheet.

How to Budget – 7 Simple Steps to a Successful Budget

What is a Budget?

In short, a budget is a plan that helps you manage money.

It helps you determine how much cash flow is available for spending, saving and bill payments.

Furthermore, a budget acts as a guide to help you reach your financial goals—short term and long term financial goals.

Why Create a Budget?

Whether you are trying to reach financial independence, buy a house, or save for a trip, every great financial plan begins with a great budget.

Maintaining a budget will help you reach your financial goals. It can also alleviate stress, prevent spending problems, and stop you from feeling overwhelmed about money.

Furthermore, budgeting clarifies where your money is going. It is essential to know how your money is being spent in order to build up net worth, save money, invest, or to have extra money available for emergencies.

Creating a budget allows you to save money on any level of income. In turn, you can build additional income streams that provide even more money to budget.

Related post: View yourself as a Business to Save Money

What to consider before creating a Budget

The most important factor to consider when creating a budget is why you are creating a budget. You must know what you want to accomplish financially.

Examples include paying off debt, saving for a house, saving for a trip, saving money to invest, saving for financial independence, or just to take control of your finances.

In addition, you must know your financial liabilities and expenses. Every single one. What are your fixed expenses, debt obligations, and you must know how much you earn each month. It’s important to remember every single detail for a successful budget to work.

Once you know the answers to why you want to create a budget, you are ready to begin.

You don’t need to be a Spreadsheet Expert

Before going any further, you should know that this post does not teach how to use spreadsheet software. This post focuses on the basics of creating a budget, such as categories, expenses, and how a chart looks. I have included screen shots from Apple Numbers.

For the sake of this post, I created a brand new budget from scratch to see how long it would take—it took 20 to 30 minutes at most.

Once the frame work is set up, it is very easy to enter the numbers to keep track of your finances. It’s also simple to alter the formulas if your financial situation changes or if your income fluctuates.

Regarding the calculations, the only calculations you need to know involve multiplication and subtraction. (Please see formulas below)

As long as you have a basic understanding of computers and Microsoft Office, you will be able to create a spread sheet.

And I’m by no means an expert on spreadsheets. I took a 4 month course on Microsoft Excel as part of my curriculum in College, and I completed a few online courses while working at my previous employer. But other than that, I figured it out on my own.

Calculations

There are only two calculations you need to know to learn how to budget.

First off, to begin any calculation in a spreadsheet, simply press the equal (=) sign.

Upon entering the equal sign, the spreadsheet will allow you to enter a formula or click other rectangles within the spreadsheet.

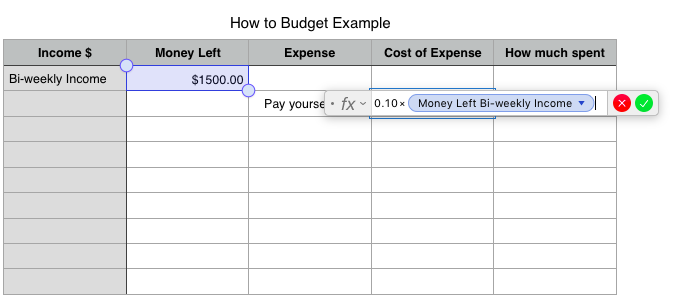

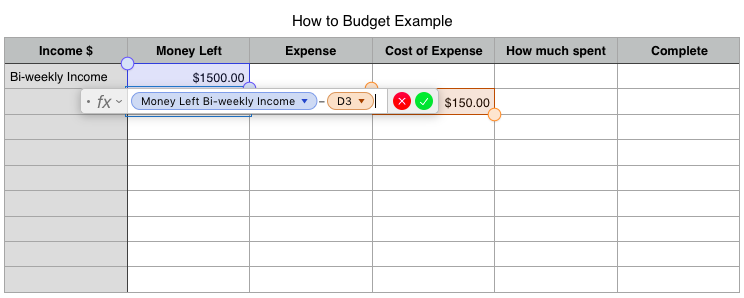

To calculate a percentage of your total income, simply press “=” then enter the following:

0.10*income

However, for the income part of the calculation, you can just select the corresponding rectangle as show below:

The other calculation to know is basic subtraction. After pressing “=” to begin the calculation, you just need to select the rectangle that represents the amount of money you are starting with, then click the minus sign (-) followed by the rectangle that represents the expense amount you are trying to subtract.

How to Budget

Step 1 – Calculate Income

The first thing to know when figuring out how to budget is your total income.

So, take a look at your recent pay stub to look for your gross income or net income. If you are salaried, it is easier because your pay is the same every two weeks. But if your income fluctuates, you may have to base your budget on your average income.

Although some books I have read focus on gross income, I base my budget and savings on net income, because that’s how much money actually hits my account. I don’t care about gross income because I don’t see it.

After you have determined how much you earn bi-weekly, monthly, and yearly (if an average is necessary), it’s time to figure out expenses.

Step 2 – Calculate Expenses

Calculating expenses is more challenging than calculating income, since there are so many different expense categories.

If this is your first time creating a budget, it may be wise to track your expenses for an entire month before attempting to create a budget.

Anyways, I covered most of the basic categories in my example of how to budget.

The most basic categories to include are the following:

- Shelter (mortgage or rent)

- Food (groceries and eating out)

- transportation (how do you get to work)

From there, you can focus on how much to pay yourself first, debts, and other miscellaneous expenses.

Just track every single expense no matter how small it is.

Step 3 – Analyze Current Financial Situation

How you set up your budget and manage your money should depend on your current financial situation.

If you have debt, depending on the interest rate, paying off debt should be your main priority. Obviously paying off debt is not the most entertaining option, but paying off debt will lead to more cash flow.

On the other hand, if your debt is paid off, it depends on what your financial priorities are. It depends on how much you want to spend on travel, personal hobbies, how soon you want to retire, how expensive your taste is, if you want to buy a house, or reaching financial independence.

After analyzing your debt obligations and financial priorities, it’s time to set up your savings or debt payoff goals.

Related post: Financial Goals for 2020 | A Financial Conundrum

Step 4 – Set Savings Goals or Debt Payoff Goals Accordingly

Now that you have analyzed your financial situation and know how much income you generate, you are prepared to set your savings or debt payoff goals.

For your savings goals, I would recommend that you pay yourself first. Just pay yourself an affordable percent of your income. Just remember, if you can save 50% of your income, you can afford a year off for every 2 years you work.

In regards to debt payoff goals, it’s usually best to get rid of the highest interest rate debt first, since it costs the most in interest. However, sometimes eliminating a small debt is motivating.

Step 5 – Set up Spreadsheet (the X Axis across the top)

Once you know your net income and expenses, it’s time to create a chart in Microsoft Excel or on Apple Numbers to budget your money.

Personally, I use Apple Numbers because I am a MacBook Air user. But Microsoft Excel is still the more advanced spreadsheet software overall.

To begin, you must lay out the categories across the top (X axis).

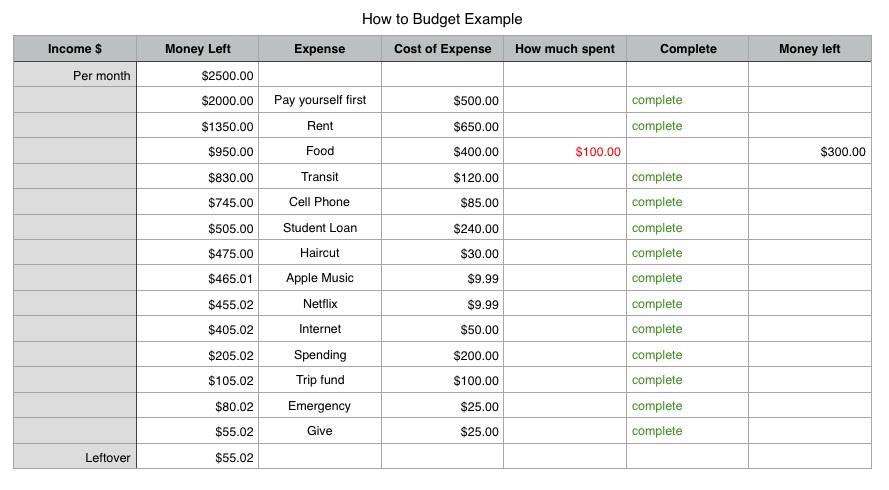

So open a new file on whatever spreadsheet system you are using and begin. Here is an example of my categories:

Across the top, you can see income, money left, expense item, cost of expense, how much spent, complete, and money left 2.

Each category has its own specific purpose:

Income: The amount of income earned from jobbing, owning a business, or from owning assets.

Money left: The “money left” category is used to determine how much of your income is left after the expenses. Basically, this is the most important column of all, as it lets you know how much money is left.

Expense item: The name for the expense. It’s important to know all your expenses to keep track of where money is going.

Cost of Expense: The dollar amount that each of the expenses on the list costs.

How much spent: For items such as groceries, the money allowed for spending may not all be spent in one grocery shop. So, in order to know how much is spent, I keep track of how much was spent on food under this category. The total from this category will subtract from the allotted amount for food to know exactly how much is left to spend on a day by day basis.

Complete: This category exists as a checklist to confirm that the expense has already been paid. This is a personal preference.

Money left 2: This category connects to the “Cost of expense” and “How much spent” categories, as it is the amount of money left after subtracting the “how much spent” category from the “cost of the expense.” It exists so I can track my spending on groceries and food daily.

The Y Axis (going down)

The Y axis is primary used to track how much money is left after expenses.

If you take a look at the example of a budget chart I created above, you can see that there is less money left after each expense.

This is the main reason why it is best to use a spreadsheet sheet for successful budget—it automatically calculates how much money you have left so there is no room for error.

Step 6 – Enter in the Numbers and Formulas

Congratulations!

If you reached this step, you set up the framework for your budget.

Now that the X and Y Axis are set up, and now that you know your financial goals and expenses, it’s time to enter the numbers.

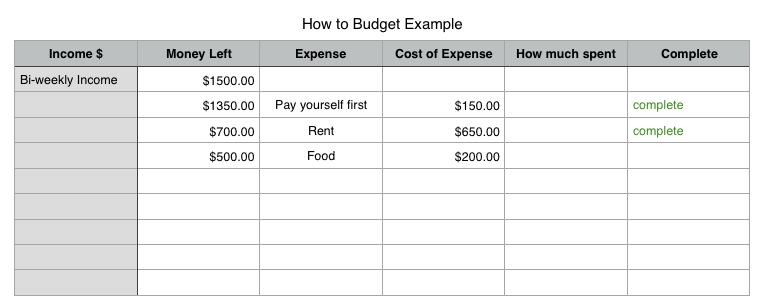

In my opinion, the first category you should start with is yourself. You should always pay yourself first.

Of course, how much you pay yourself first is up to you. I would suggest at least 10% of your net income if possible. But even starting with 1% and moving up slowly is a good idea.

Second, it’s probably best to get the larger fixed expenses that are unavoidable out of the way. So, that means rent or mortgage, food, and transportation costs.

After you have entered the unavoidable expenses like food, shelter, and transportation, focus on debt.

Because as most personal finance experts would tell you, the interest paid on debt drains your cash flow. It is a reverse cash flow machine.

After debt, the categories become more customizable. Perhaps it’s subscription services, internet, cable, cell phones, or just spending. The main thing to remember is to include every single category, even the smallest expenses.

Saving money becomes easier if all your expenses are accounted for.

Step 7 – Review your Budget often

As soon as you become a real adult and have to fend for yourself, you soon realize that nothing is perfect. It’s impossible to maintain perfect control over life.

In the same way, it’s impossible to create the perfect budget.

Different groceries are on sale from week to week. Special events come up. And sometimes life just gets in its own way.

Because of life’s unpredictability, it’s important to review your budget regularly. In my case, I try to review it daily or every time I visit a grocery store. I even budget every time I buy a coffee, or I try to.

Overall, I would recommend that you stay on top of your budget by budgeting at least a month or two paydays into the future.

Related post: 5 Expenses to Cut-Out to Increase Cash Flow

How to Budget – Concluding Thoughts

As long as you understand basic addition and subtraction math, and if you possess basic computer skills, it’s possible to create a budget using the same steps I have shown.

Therefore, it is possible for anyone to create a budget to save money.

In summary, here is how to budget:

- Calculate Income

- Calculate Expenses

- Analyze current financial situation

- Set savings goals or debt payoff goals

- Set up spreadsheet

- Enter numbers and formulas

- Review your budget often.

Moreover, budgeting and paying yourself first are simple habits that anyone can build.

I have personally used these budgeting tips to pay down my own student loan and to save money to fund my dividend income updates, so I hope you find them useful!

I am not a licensed investment or tax adviser. All opinions are my own. This post contains advertisements by Google Adsense. This post also contains internal links, affiliate links, links to external sites, and links to RTC social media accounts.

Earn passive income through dividend investing with RTC’s link below ($50 in free trades):

Connect with RTC

Twitter: @Reversethecrush

Pinterest: @reversethecrushblog

Instagram: @reversethecrush_

Facebook: @reversethecrushblog

Email: graham@reversethecrush.com

Marketing a Blog – How to Market a Blog on Social Media – Daily Checklist

Marketing a Blog – How to Market a Blog on Social Media – Daily Checklist