Welcome to my monthly savings report for March 2019.

I decided to start documenting how much money I save each month in January.

The purpose is to motivate myself to save more, and because I wanted to show that anyone can do this. I’m really not saving an impressive amount, yet…

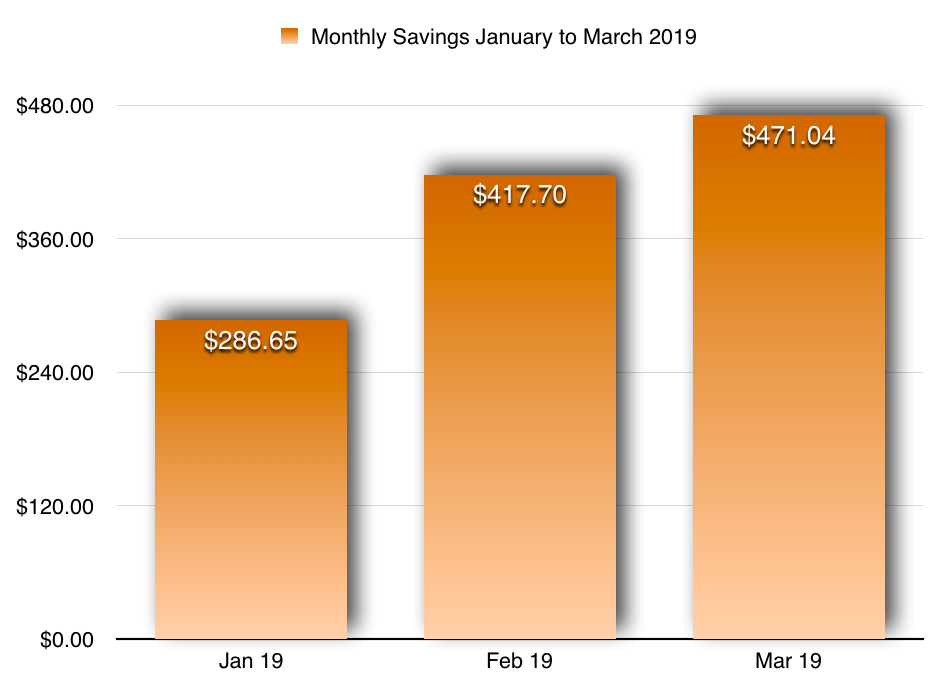

But I am improving every single month and I can prove it—March was the 3rd month in a row that my savings increased.

$471.04 Saved in March 2019 | $1,175.39 Saved Year to date.

I saved $471.04 during the month of March. This works out to $53.34 more than last month.

In total, I’ve saved $1,175.39 year to date now. Although I’m happy to reach 4 figures, it’s still not enough!

As I alluded to in last month’s report, I need to save a lot more to reach financial independence any time soon (10 to 15 years). I’m not on pace right now. I’m losing the race against time.

Furthermore, saving money has less of an impact as the size of your portfolio increases. For example, daily fluctuations of my holdings can exceed the amount I’m able to save in 2 weeks.

As such, it’s important to maintain a long term perspective and view saving and investing as a habit.

Related Post: Make Saving Money Your Career

Allocation

$296.88 went to a non-registered investment account that is intended for Canadian dividend stocks.

$127.72 of my monthly savings was allocated to my TFSA. The money in my TFSA is mostly intended for Canadian dividend paying stocks. 90% of it is for Canadian dividend stocks, while the other 10% is available to speculate longterm on cannabis stocks.

$23.22 was contributed to a high interest savings account.

$23.22 was contributed to my RRSP, which I use to purchase USD stocks. I’m not contributing much money to my RRSP right now because USD stock prices are high, and because it doesn’t make sense to contribute a lot based on my income. I am essentially contributing an amount that is similar to the tax credit I used to receive for taking transit.

Concluding Thoughts

By the way, the money discussed in this report does not include any vacation savings. I am saving a small amount for that, too, through payroll deductions. I would’ve exceeded $500 if I included that amount.

As a cautionary statement, though, I am planning a small trip in April that could impact my savings. I am hopeful that I will still be able to increase savings, but I might have to save less to afford the trip.

In summary, another $471.04 was saved for financial independence in March 2019. I’ve saved $1,175.39 so far in 2019.

As mentioned earlier, it’s nice to have saved 4 digits so far this year. It’s proof that I’ve done something right. However, I still need to save $4,824.61 more in order to meet the $6,000 target set. With 9 months to go, I’ll need to save an average of $536 per month. It may not seem like I’ll be able to based on the first 3 months this year, but I am certain that it is achievable.

I’ll just have to keep my budget in focus and keep paying myself first.

Connect with RTC

Twitter: @Reversethecrush

Pinterest: @reversethecrushblog

Instagram: @reversethecrush_

Facebook: @reversethecrushblog

Email: graham@reversethecrush.com

I am not a licensed investment or tax adviser. All opinions are my own. This post contains advertisements by Google Adsense. All links in this post are internal links and links to RTC social media accounts.

Why Dividend Investing is my Main Investment Strategy

Why Dividend Investing is my Main Investment Strategy